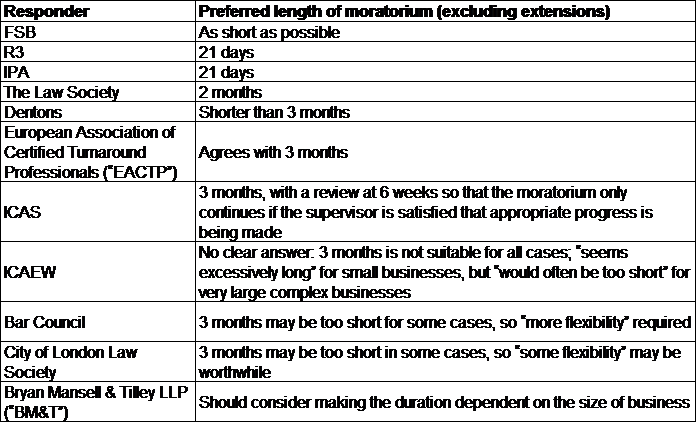

It would be a mistake to assume that we don’t need to think about the revised SIP3.2 until 1 April. It applies to all nominee appointments from 1 April 2021, so in view of the lead time on preparing CVA Proposals, you may well find that you already have engagements that need to comply with the new SIP3.2.

In this article, I look at the practical effects of the changes to SIP3.2.

Firstly, though, I should apologise for maligning the ICAEW. In my last blog, I’d said that they had not formally issued the revised SIPs, but I’d overlooked an email that hit my inbox two days before I posted my article. The IPA finally issued the SIPs on 10 March 2021… so if you’re an IPA member who has already issued an unchanged advice letter to deal with a nominee appointment that you expect to get after 1 April, I suggest that you have a very good excuse why the letter didn’t comply with the new SIP.

The revised SIP3.2 (E&W) can be found at https://www.icaew.com/-/media/corporate/files/technical/insolvency/regulations-and-standards/sips/england/sip-3-2-company-voluntary-arrangements-england-and-wales.ashx

More Ethical Taglines

There are several new references in the SIP to acting professionally, objectively etc. In practice, these don’t affect how IPs work, as I’m sure that your Ethics Checklists and periodic case reviews already keep these requirements in the frame. The SIP3.2 additions just seem to be another cudgel that an RPB may wield if they see unethical behaviour, although I’m not sure why the Ethics Code needs an escort.

Instead, let’s focus on what you need to change to comply with the new SIP.

“Additional Specialist Assistance”

The SIP requires the IP to have procedures in place to ensure that, at each appropriate stage of the process, the company/directors are informed about:

“whether and why the company will require additional specialist assistance which will not be provided by any supervisor appointed, including the likely cost of that additional assistance, if known”

On a similar theme, the Proposal must contain information on:

“any additional specialist assistance which may be required by the company which will not be provided by any supervisor appointed, and the reason why such assistance may be necessary.., the cost of any additional specialist assistance”

What do the drafters have in mind here? Perhaps they are thinking about restructuring professionals. “Additional specialist assistance” could also encompass other instructions, for example where the company expects to deal with something outside the ordinary course of business, such as selling assets… or dealing with a legal matter… or refinancing… or…

Of course, it makes sense to ensure that the directors are prepared to factor in such additional costs, but I am not sure I understand what this has to do with the creditors: if the Proposal sets out what net proceeds or contributions will come into the CVA together with sensible forecasts where appropriate – and further details if the IP’s firm is to receive any additional payments (as was already required by SIP3.2) – then isn’t that enough to enable them to assess the Proposal?

Changes to Advice Letters and Interview Records

In addition to covering off any additional specialist assistance, advice letters and/or interview records must now explain the directors’ responsibilities and role both before and during the CVA – “during” is new.

Instead of requiring a “face to face” meeting with the directors, the SIP now requires the initial meeting to be “in person (whether a physical meeting or using conferencing technology)”. For sole directors, would a telephone meeting be acceptable..? In any event, it might be useful to add to your interview record the method used.

More Strategy Notes

The SIP adds some new strategy note requirements, which might also be incorporated into interview records. It requires:

- “A detailed note of the strategy, outlining the advantages and disadvantages of each option”, which was previously only required for Administrator/Liquidator Proposals

- “…including the impact of trading within a CVA for a prolonged period and the continued viability of the business during that period” – this is new and makes sense to me: it is of course sensible to manage the directors’ expectations, make them fully aware of how tough it can be to trade on in a CVA. CVA companies may have some protection via S233 and S233A, but practically I suspect that most creditor suppliers make CVA companies go through pain. The SIP also requires:

- Creditors to be “given adequate time to consider what is being planned as regards the CVA”. I find this odd: what are the RPBs’ expectations? In the ICAS webinar (http://ow.ly/tcGU50DKuCp), David Menzies suggested that IPs should document why the period of time given to creditors to consider the CVA is adequate, including factors such as the delivery time and the time creditors would need to get advice. But the company is insolvent, it is probably continuing to trade under difficult and uncertain circumstances, surely the approval of a CVA should be pursued as quickly as possible, for creditors’ sakes as well as the company’s? The Rules put a narrow timescale on the process – effectively between 14 and 28 days from delivery of the nominee’s report – so presumably the legislators felt that 14 days (post-delivery) was adequate time for creditors, doesn’t this satisfy SIP3.2?

Signposting Sources of Help

Something else to record on the strategy note might be your consideration of “signposting sources of help” “where creditors may need assistance in understanding the consequences of a CVA”.

In his webinar, David Menzies recommended that IPs should document their consideration of the creditor composition, such as their knowledge, experience and skills, and especially if the IP is not going to be signposting creditors to sources of help. He also suggested that we gather details of potential sources of help – generic and sector specific – that could be signposted to.

Ok, a generic one is the R3’s site at http://www.creditorinsolvencyguide.co.uk/, which I expect many of us added to our initial creditor letters years ago. Other than that, where would you signpost creditors to?

The elephant in the room is the British Property Federation, which was represented on the SIP3.2 working group. Additions to the Proposal’s contents listed below strongly suggest that the BPF had quite some influence over the revised SIP. True, the BPF provides guidance for landlords who receive a CVA Proposal, but I question whether it is helpful to the process to recommend that landlords issue a 33-point wishlist to nominees as “a standard document… if they do not feel they have been provided with the requisite information” (https://bpf.org.uk/media/2319/cva-creditor-friendly-document-09102019.pdf).

What about employees? Ok, employees rarely have much more than contingent claims that won’t crystallise, but particularly as they could find that not all their claims would be covered by the RPS in the event of an insolvency process following the CVA, it would seem appropriate to consider giving them access to guidance. However .gov.uk’s coverage is poor. https://www.gov.uk/your-rights-if-your-employer-is-insolvent simply lists CVA amongst the insolvency processes and states that employees might be able to make claims to the government.

Well, that’s two creditor groups that might not be helped with any existing resources. It seems that the JIC has put the cart before the horse on this one.

Much More Required in Proposals

The new SIP adds several new items to the Proposals’ tick-sheet:

- Additional specialist assistance, as explained above;

- The alternative options considered, both prior to and within formal insolvency by the company;

- An explanation of the role and powers of the supervisor;

- Details of any discussions with key creditors;

- Where it is proposed that certain creditors are to be treated differently, an explanation as to which creditors are affected, how and why;

- An explanation of how debts are to be valued for voting purposes, in particular where the creditors include long term or contingent liabilities;

- An explanation of how debts that it is proposed are compromised will be treated should the CVA fail;

- The circumstances in which the CVA may fail; and

- What will happen to the company and any remaining assets subject to the CVA should the CVA fail.

Although I dislike the way SIP requirements grow and grow, most of the above additions are not disastrous and in fact several are probably addressed in most CVA Proposal templates already. At least two of the new requirements are clearly targeted at multiple landlord CVA Proposals, which one would hope are already being well crafted with the assistance of solicitors.

One of the new requirements has got us puzzling.

How to Value Votes

Firstly, is it possible to define how votes will be valued for the S3 process other than as set out by legislation and case law precedent? If the chair/convener were to value votes in any other way, wouldn’t it give rise to grounds for a challenge of material irregularity?

Secondly, what can be the point of adding to the Proposal terms setting out how claims will be valued for voting in the S3 process, when the Proposal does not take effect until after the vote has been determined? A Proposal’s terms cannot have any effect on what happens before it is approved, can it?

Presumably, therefore, the regulators only expect Proposals to set out how votes would be valued in decision processes during the course of the CVA… although that’s not what the SIP says.

But what kind of explanation do the regulators expect? If it is proposed that votes be valued by applying the Rules for statutory decision processes in CVA, e.g. by following R15.31(1) that votes will be calculated according to the claims as at the decision date and R15.31(3) that debts of unliquidated or unascertained amounts will be valued at £1 unless the chair/convener decides to put a higher value on it, is this sufficient explanation? Or do the regulators expect Proposals to set out how every single claim (especially the uncertain ones) will be valued and at every stage of the CVA, e.g. before adjudicating on claims for dividend purposes and then after having paid a dividend? What about if there is new case law that takes things in a different direction? Should a supervisor simply consider themselves bound by what the Proposal (and perhaps as modified!) dictates?

After Approval

AND breathe. In comparison, the post-approval additions don’t look too grim.

The SIP adds to the supervisor’s post-approval duties:

- Sources of income of the associates of the IP in relation to the case must be disclosed (the old SIP restricted it to the IP’s and their firm’s income);

- If the CVA costs have increased beyond previously reported estimates, not only should the increase be reported, but also “an explanation of the increase” should be provided;

- When a CVA concludes or fails, the supervisor should ensure that the company is dealt with appropriately in accordance with the CVA Proposal (presumably where this is in the supervisor’s power?); and what is to happen should be reported to creditors.