My second post on the Small Business Enterprise and Employment Bill focuses on the proposed changes to the Insolvency Act as a consequence of the Red Tape Challenge… with a couple of sneaky additions thrown in.

Changes to the Insolvency Act 1986

The Red Tape Challenge proposals require changes both to the Act and the Rules. Therefore, this Bill is not the whole story and many of the practicalities of the new processes will only become evident when the Insolvency Rules are changed.

The Insolvency Service’s current targets on the Rules consolidation exercise appear to be finalisation of the statutory instrument in October 2015 so that it has an effective date of April 2016.

The Bill’s Impact Assessment (“IA”) summarises the changes as follows:

1. “Removing meetings of creditors as the default position in insolvencies

2. Abolition of final meetings

3. Removal of requirement for liquidator to be present at a S98 meeting

4. Opting out of further correspondence

5. Administration extensions

6. Allowing an office-holder to pay a dividend in respect of a debt of less than £1,000 without the need for the creditor to submit a formal claim

7. Removal of requirement to seek sanction for certain actions in liquidation and bankruptcy

8. Crystallisation of Scottish floating charges

9. Abolition of Fast Track Voluntary Arrangements

10. Official Receiver to be appointed trustee on the making of a bankruptcy order

11. Clarification that a court application under paragraph 65 of Schedule B1 is not required where an administrator intends to make a prescribed part payment to unsecured creditors

12. Clarification that a progress report must be issued to creditors where the liquidator changes within the first year of a CVL

13. Alignment of the time limit for an appeal against the outcome of an IVA where there is no interim order with that where there is an interim order in place”

“Deemed consent” and non-physical meetings

The savings that will result from complete removal of “physical” meetings seem to be built on the premise that all IPs are charging room hire of £64 and 1.5 hours of administrator/manager time each time a meeting is “held”. Although the vast number of circulars still refer to a place and time for meetings, I suspect that rarely does this involve any more cost than if the business were conducted by correspondence.

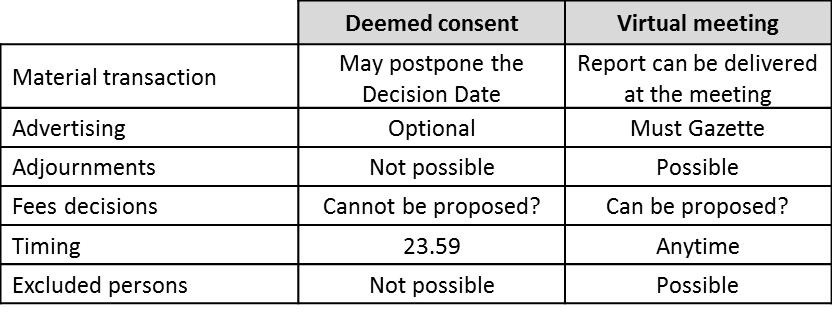

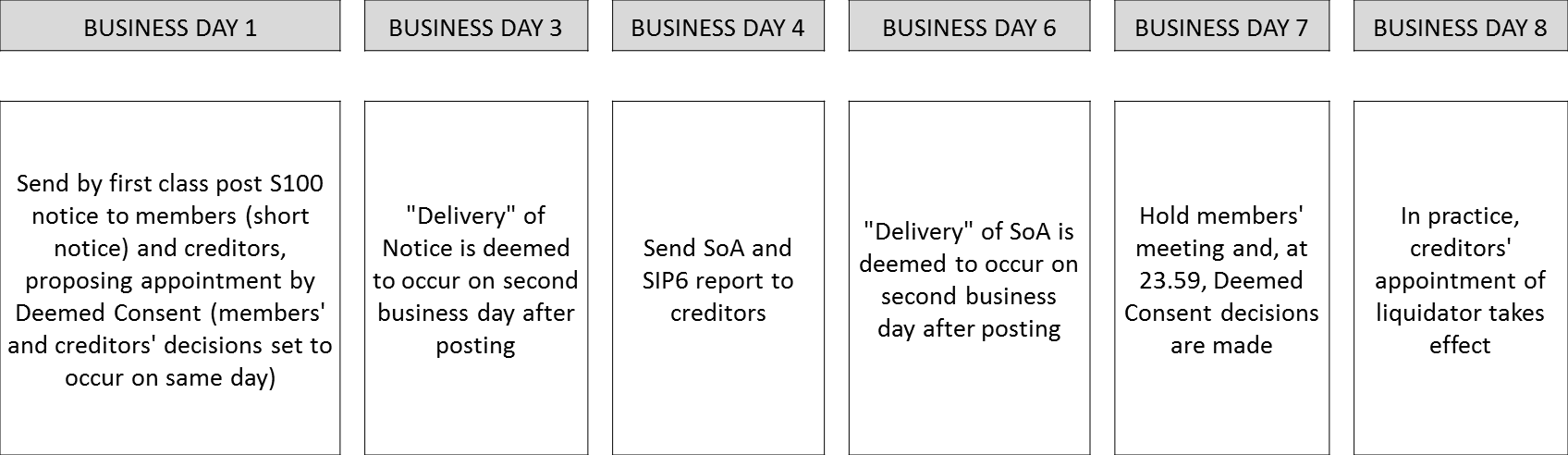

Firstly, the Bill introduces a “deemed consent procedure” (S110 and 111) that seems to work like this:

• The office holder provides creditors with written notice of his “proposed decision” on a matter.

• If less than 10% (or perhaps “10% or less” – the IA does not make it clear and the Rules will prescribe this) of total creditors by value object to the proposed decision, the creditors are treated as having made the decision.

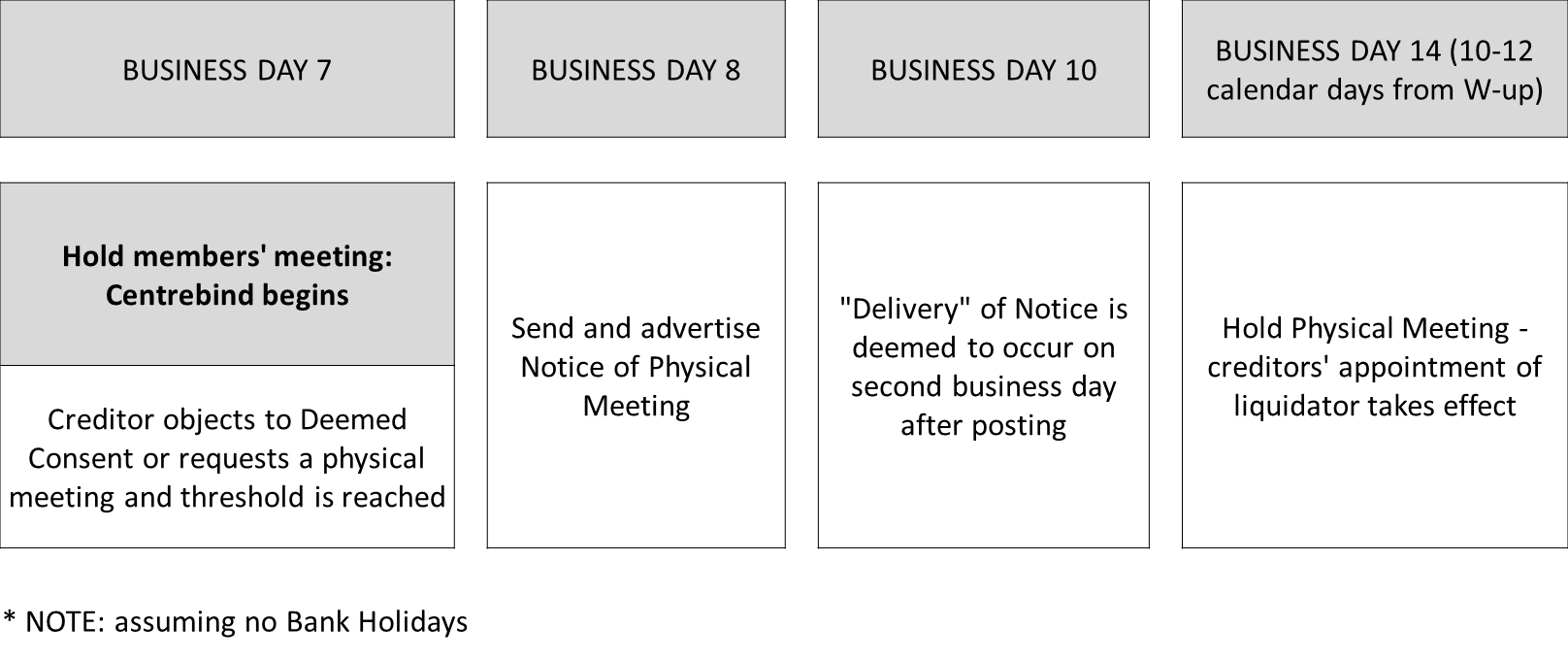

• If more than 10% (or “10% or more”) object to the proposed decision, then the office holder must follow a “qualifying decision procedure”.

The Bill lists several decisions that cannot be handled by the deemed consent procedure:

• “Any matter relating to a proposal” for a VA;

• Removal of an office holder;

• “Any matter relating to the remuneration of an office holder”, which I guess will wrap in S98s and consideration of Administrators’ Proposals (unless Para 52(1)(b) applies);

• Where the court so orders; and

• “Any matter prescribed as an excluded matter by the Rules”.

The IA suggests that the process will not disadvantage small-value creditors, as “they will still have the facility to object to [the proposals] and raise any concerns with the office holder, who will in turn have a duty to consider whether deemed consent is the most appropriate mechanism to use”, which seems most odd: does the Service expect office holders to start the deemed consent process and, even if the 10% threshold has not been passed, they might decide that minority objecting creditors deserve a voice and thus they can spend estate monies in following a more inclusive decision-making process? This also seems contrary to the Bill, which states that, if less than the prescribed proportion of creditors object, the creditors are to be treated as having made the proposed decision (S246ZF(4) under S110).

The IA does point out that use of the deemed consent procedure is discretionary; it states that “office holders will be able to use their experience to identify situations where the creditors are unlikely to agree with its use” and thus go straight to an alternative decision procedure. However, the Service also waves the stick of regulatory action, if it seems that an IP has lost sight of achieving “value for money”.

The Bill’s memorandum states: “in most cases the intention is that the office holder will be able to use a process of deemed consent”. However, given the exclusions listed above, how many opportunities will there be for the deemed consent procedure in any event? How many meetings (other than final meetings, which are dealt with elsewhere) do not include a resolution on fees?

The Bill doesn’t prescribe the qualifying decision procedures – the Rules will “prescribe examples of procedures” – but the IA indicates that these will not include a physical meeting, unless 10% or more request a physical meeting. The procedures will include business by correspondence, remote meetings, and electronic voting.

Given that most meetings are convened at present to deal with the excluded matters listed above and that physical meetings will not be an option unless creditors ask for one, I really cannot see why the IA has estimated a reduction of only 50% in the number of physical meetings. It states that “50% was seen as prudent, given because this will be ‘new ground’ for office holders and creditors, who may feel decide (sic.) that they would prefer to have meetings in some cases”. Don’t you get it, Insolvency Service? How many times do we have to say it? On the whole, creditors don’t vote! Why on earth would they – in 50% of cases! – ask for a physical meeting?!

The IA states that “it is not anticipated that the time taken to undertake a virtual meeting will be any more or less than the time taken to undertake a physical meeting” – I agree – but it then states “where a physical meeting is not being held the proportion of instances where a virtual or remote meeting is held is likely to be small, given that deemed consent will be available as well as other cheaper methods”. The IA then applies a best estimate of 50% reduction in meetings, whether virtual or physical, and eliminates entirely the time costs of an estimated 1.5 hours for holding a meeting. Crazy! As is clear above, there will barely be an opportunity to use deemed consent and, as the time incurred in completing unattended meetings is mostly about collating and considering proofs and proxies and drafting minutes, these pretty-much will still need to be spent in any other decision procedure. Okay, business by correspondence will be cheaper than a physical or virtual meeting where people actually turn up, but it is not cost-free!

Is it any wonder that the Service has managed to come up with savings for this measure alone of £50 million over ten years?!

Final meetings

The IA states that the proposal “scraps all final meetings of creditors where they occur”, although the Bill (S114) provides only that the SoS be empowered to remove Insolvency Act meetings, so I think there is another step required to amend S106 etc. It is not clear whether the Service envisages that the deemed consent procedure will apply to a proposed resolution for release, or whether the draft final report simply will be issued and creditors will need to request a meeting, if they want to object to the office holder’s release.

The IA suggests that this measure will save £6 million per year (in addition to the £50 million above), based on room hire of £64 per meeting and 45 minutes of time, although, if the deemed consent procedure were necessary, it will carry with it some costs to wrap up. The Bill does not refer to any requirement to tell creditors the outcome of any attempt at obtaining deemed consent; hopefully the Rules changes will add nothing, as this would return any costs saved in abolishing final meetings.

S98 meetings

The Bill and IA seem confused over the fate of S98 meetings: are they being abolished? If not, who gets to decide how they should be held? And practically, how can such decisions be managed?

One thing is clear: the need for the company’s liquidator to be present at the S98 meeting will be removed (although it is not in the Bill, as it is a Rules provision). The IA states that “in most cases it will be an insolvency manager who has best knowledge of the intricacies of a CVL rather than the office holder themselves and it represents much better value for the creditors for that person to attend the meeting” – charming! Don’t they think that creditors will want and deserve to see the liquidator in person? The IA does acknowledge that, if there is significant creditor interest in the proceedings, suggestion of director misconduct or “negotiations that the office holder in person may wish to lead”, the IP may “feel that their presence would be necessary or beneficial”. The IA estimates this may occur in 30% of cases.

I know that some have aired grave concerns over the prospect of creditor disengagement by abolishing physical S98 meetings. Chuka Umunna MP commented on this when the Bill had its second reading – see column 922 at http://goo.gl/VGOE07.

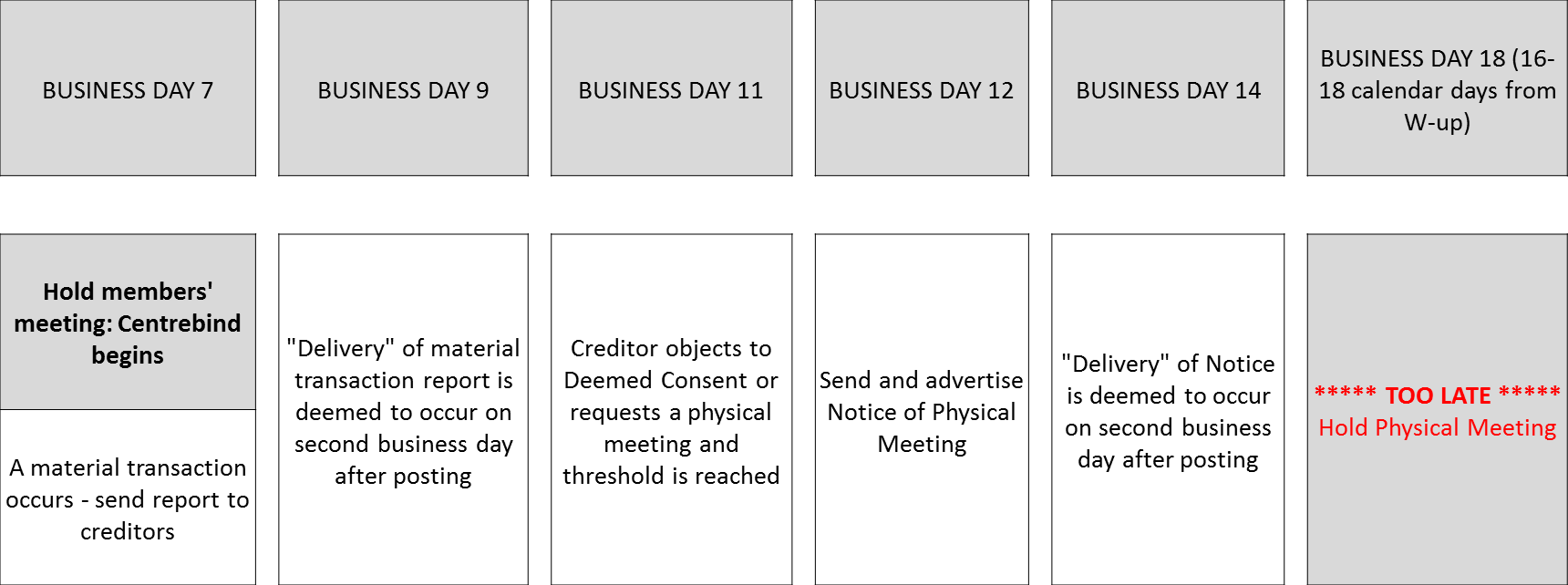

But are physical S98 meetings being abolished? The IA estimates there will be a 50% reduction in physical S98 meetings, which suggests that they aren’t. However, from my reading of the Bill, it seems that S98s will be subject to the “qualifying decision procedure” rules, which means that a physical meeting could only be held where over 10% of creditors request one, so, without this, an IP may only decide to “attend” a meeting remotely. Also don’t directors technically convene S98 meetings..? So a director who doesn’t want to face creditors – even remotely – can decide to conduct business by correspondence..?

Given that creditors only receive seven days’ notice of S98 meetings, I am not sure how a creditor’s request for a physical meeting will work practically. Presumably, directors/IPs may do well to predict cases where there is likely to be sufficient creditor interest and set up a meeting room in advance (although this will be wasted if the requisite creditors do not request a meeting). Otherwise, they could be looking at expensive last-minute conference room bookings – and you would need to give timely notice to all creditors of the venue – or a postponed S98 meeting, albeit not for long given the need to get on with the liquidation and the Centrebind restrictions.

So much for saving costs!

Creditors’ circulars

The Bill provides (Ss 112, 113) that creditors may opt out of receiving correspondence from office holders (excluding notices of (proposed) distributions, which presumably include notices of intended dividends).

Again, I think the Service has over-estimated the savings to be made: personally, I cannot see their assumption of 20% of creditors deciding to opt out becoming reality, although apparently “a representative of a leading firm of insolvency practitioners, a partner in a large regional firm, and a major creditor representative all said that they agreed that the assumption was reasonable and two of them thought the 20% figure to be conservative”, so what do I know..? I also note the IA assumption that no creditors will opt out where the OR is in office: if this provision is such a cost-saver, why is it only being imposed on IPs? They have also provided no provision for the costs to the office holder of managing two creditor databases.

What I want to know is: where has the other Red Tape Challenge proposal gone? If the Service is serious about IPs’ saving costs, then they should progress the proposal to allow office holders to post everything on a website without the need to write to each creditor every time notifying them that the document had been released. Maybe this will turn up in the Rules revision…

Extending administration extensions

Para 76(2)(b) of Schedule B1 is to be changed so that an administration may be extended by up to one year by consent (S115).

It is a shame the Service has not taken this opportunity to change the consent requirements, so that it does not require the administrator to seek the approval of every secured creditor, irrespective of their recovery prospects. Oh well. This may mean that the Service’s prediction that all administrations set to last up to two years will be extended by consent in future may prove to be an over-estimate also.

Dividend processes

Ss119 and 120 of the Bill provide for creditors who have not proved small debts (to be prescribed, although the IA proposes a threshold of £1,000) “to be treated as having done so”. The IA points out that, as with any proving creditor, this does not stop the office holder asking for further evidence from the creditor if thought necessary, although it states that this measure will “permit the insolvency office holder to rely upon the debtor’s own records”. Also, a creditor can always submit a proof, if it is owed more than the debtor’s records indicate.

I must admit that I have often struggled with the office holder’s duty as regards adjudicating on claims and I have even more difficulty with it in this “value for money” world: on the one hand, an office holder is expected to be diligent to ensure that he distributes the estate’s monies to those who are entitled to it; however, on the other hand, every minute he spends on scrutinising claims, asking for, and examining further evidence, eats away at the funds available to distribute. I guess this provision sets out more clearly the government’s expectation: just take small claims as read… unless you have reason to doubt them, e.g. if you think that the director who swore the SoA has added all his friends and neighbours to the list of creditors.

A Red Tape Challenge proposal that would really help put this measure into context is that small dividend payments – £5 or £10 were mentioned – would not be sent to individual creditors, but would be pooled for use by the disqualification unit or the Treasury. If this also were introduced, then, yes indeed, don’t waste any time considering whether to admit small claims, as the chances are that those creditors will not see their dividends anyway. However, this proposal hasn’t made it to the Bill. Is it another one for the Rules or will we never see it again..? (UPDATE 02/11/2014: I understand this proposal has now been dropped, as the Service had received advice that it would prove too contentious to deprive certain creditors of the right to receive a dividend, however small that might be.)

The Bill includes two measures affecting administration distributions. The IA describes them as clarifications and as removing ambiguities, although personally I think that the provisions change the Act, which seems pretty clear-cut to me.

S116 contains two parts:

• To Paragraph 65(3) will be added the power to distribute the prescribed part in an administration.

• Paragraph 83 will include a further restriction on moving from administration to CVL: this will only be possible where the administrator thinks that a non-prescribed part distribution will be made to unsecured creditors.

It is a shame that Schedule B1 of the Act is not being amended so that dividends generally can be paid through administration. The IA hints at why this is not considered appropriate: it states that liquidation “provides for more engagement” of unsecured creditors. Personally, I see no difference in creditor engagement in administrations and liquidations: there are the same powers to form a committee and to approve fees (as we are not talking about Para 52(1)(b) cases here), and the changes to liquidators’ powers mentioned below bring the office holders’ needs to seek sanction on a par. The IA has estimated a cost of £8,250 on converting an administration to liquidation, so why not save by eliminating the need to move to liquidation?

Pre-packs

S117 of the Bill is the Dear IP 62 threat to “ban ‘pre-pack’ administration sales to connected parties if certain criteria are not met”. The Bill’s memorandum elaborates, referring to Teresa Graham’s recommendations: “Clause 117 is in response to the recommendation to take a legislative power to legislate in the event that the recommendation to establish third party scrutiny is not adopted on a voluntary basis… It is considered that by taking a legislative power, this will act as an incentive to encourage connected parties to adopt the voluntary proposals set out in the Graham Review”. Hmm… I can’t see that the threat of future legislation is going to matter one jot to connected parties presently contemplating a sale! However, “the Government is fairly confident that voluntary reforms backed by this ‘backstop’ power will act as sufficient incentive to change behaviours and so it will not be necessary to exercise the power.” I know that R3 and others are working frantically to see what can be done with the Graham recommendations and I will not list my own views and concerns, as there have been plenty of other loud critics.

The Bill empowers the SoS to make regulations “prohibiting or imposing requirements or conditions in relation to the disposal hiring out or sale of property of a company by the administrator to a connected person in circumstances specified in the regulations”. Note that regulations may not be limited to pre-packs, but may affect any transaction involving a connected person (which is also defined by the section), whenever they occur and however large or small the property transferred. This fits in with Teresa Graham’s recommendations, although I haven’t seen any commentary refer to this wider scope.

S117 provides that, in particular, future regulations may require approval (or provide for the imposition of requirements/conditions) by creditors, the court, or “a person of a description specified by the regulations”.

Other fixes

The Bill also contains:

• S107: the proceeds of claims or assignments arising from Ss213, 214, 238, 239, 242, 243, and 244 are not to be available for floating charge holders, i.e. they will not be part of the company’s net property. I believe that some have expressed concern over this, but doesn’t this simply put case precedent into the Act?

• S108: liquidators may exercise any of the powers in Parts 1 to 3 of Schedule 4 of the Act without sanction (S109 provides similarly in relation to trustees and Schedule 5)… although I’m wondering why the Parts need to exist at all.

• S118: provides that, when an administrator of a Scottish company obtains permission from the court to pay a dividend to unsecured creditors, floating charges crystallise.

• S121: the OR will become trustee on the making of a bankruptcy order (if an IP isn’t made trustee at that time). The IA explains that the motivation for this is to improve the efficiency of asset realisations by not restricting the OR’s immediate activities only to protecting the estate. I can see some value in having the bankrupt’s estate vest in the OR immediately on bankruptcy, avoiding some of the confusion illustrated in the Pathania v Adedeji case (http://goo.gl/AcktAk), although there is obvious concern that this process disenfranchises creditors, as this erodes creditors’ opportunities to make a decision on who they want to administer the estate.

• S122: changes S262(3)(a) of the Act so that the 28 day time period for challenging an IVA meeting decision counts from the decision where there is no interim order and from the filing of the report to court in interim order cases… although I’m wondering why the time of the meeting’s decision could not work for all cases; it’s hardly “alignment”, as the IA suggests.

• S124: removes reference to producing progress reports only for (E&W) VLs that last longer than one year. This deals with the nonsensical position that, if the liquidator changes during the first year, it seems that he must predict if the case will last longer than one year in order to decide whether to issue a progress report on the change-over – an issue highlighted by Bill Burch (http://goo.gl/6K4a4E) – although it does not deal with the unnecessary costs of issuing progress reports mid-year and the re-setting of deadlines caused by changing liquidators. Courts usually deal with these matters in block transfer orders, but let’s hope that the revised Rules will effect a change.

That’s almost the whole of the Bill’s insolvency measures covered. It just leaves the provisions impacting on IP regulation… for another day.