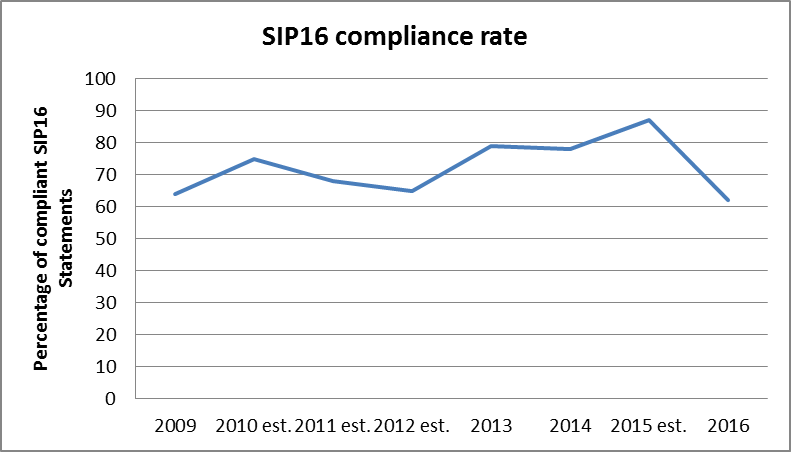

I think we’ve all shared in the pain of SIP16 compliance. We’ve tried really hard, haven’t we? So why is it that the wholly-compliant rate dropped from 87% in 2015 to 62% last year? Where are we going wrong?

In this blog, I air my suspicions about the stats, not only on SIP16 compliance, but also on the changing profile of pre-packs and the role of the Pool, as presented in the Insolvency Service’s and the Pre Pack Pool’s 2016 Reviews. Yes, I know I’m a little late on this story (I blame the 2016 Rules!).

The Insolvency Service’s 2016 Review of IP Regulation can be found at: https://goo.gl/Jkwz19

The Pre Pack Pool’s 2016 Review is at: https://goo.gl/fPEXTe

SIP16 Compliance Rates Fall Back to Square One

There has been a significant drop in the reported rate of SIP16 compliance – at 62% of 2016’s SIP16 statements considered wholly compliant, it is the lowest annual rate on record (note: several years are estimates because not all SIP16 statements received were compliance-reviewed):

Why is this? It’s true that it takes time to adapt to a new SIP and this is bound to hit compliance, but is this the whole story? Or has the shift of the job of reviewing SIP16s from the Insolvency Service to the RPBs introduced an element of inconsistency into the process?

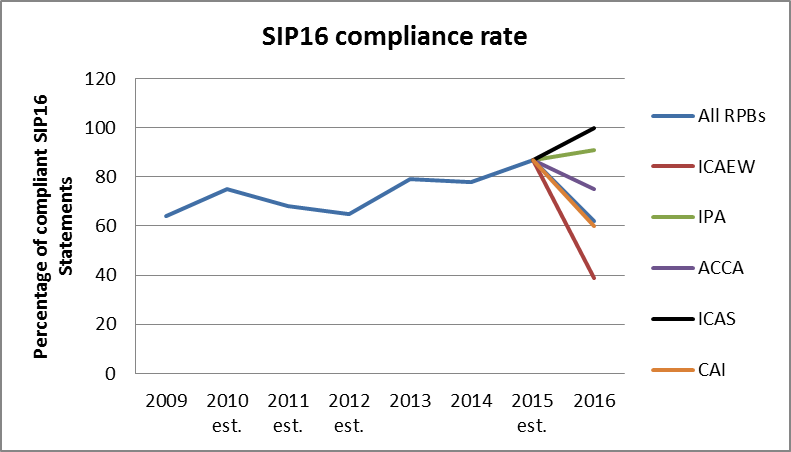

Let’s drill down into the overall compliance rate of 62% to see how the rate varies from RPB to RPB:

As you can see, the rates range from ICAS’ 100% of SIP16 statements wholly compliant to the ICAEW’s 39%.

I consider it highly unlikely that ICAEW-licensed IPs are in reality far worse at complying with SIP16 than other IPs, so this indicates strongly to me that there is a great diversity in the standards being applied. Given that the ICAEW reviewed 54% of all SIP16s received last year, it’s not surprising that the overall compliance dropped from 2015’s 87% to 62%.

The Insolvency Service’s Review does not help us to understand what might be behind the non-compliances, although it gives us some comfort. It states: “for the vast majority of non-compliant statements, the breach was not deemed to be serious and was merely of a technical nature”.

The ICAEW has published some feedback on their reviewing (Feb 2017, available to their Insolvency & Restructuring Group members at https://goo.gl/YkExP7), which suggests that the following have been lacking in some cases:

- An explanation of the pre- and post-appointment roles of the IP (the ICAEW acknowledges that SIP16 does not strictly require this explanation in the SIP16 Statement, but it needs to be delivered to creditors and directors somewhere);

- An explanation of why no requests were made to potential funders to fund working capital (even if in some cases, it is obvious);

- If the business has not been marketed on the internet, an explanation why not (even if the nature of the business makes this obvious);

- An explanation of the reasons underpinning the marketing strategy (whereas some appear to have simply provided a list of what marketing has been done);

- An explanation of the reasons behind the length of time of the marketing (even if there were obviously financial pressures that limited this);

- The date of the initial introduction – not simply “in December 2016”;

- An explanation of the rationale behind the basis/bases of valuations (helpfully, the ICAEW give a clear steer on what they expect: “where you have obtained going concern and forced sale valuations, tell [creditors] that you’ve obtained valuations on both bases as you’re seeking to understand whether realisations will be maximised by breaking up the business and selling the assets on a piecemeal basis or whether it’s better to try to find a buyer for the business as a going concern”);

- If goodwill is valued, an explanation and basis for the valuation provided; and

- An explanation of the method by which consideration was allocated to different asset classes.

Given the prevalence of some apparent failures to state the bleedin’ obvious, perhaps other RPB reviewers are measuring compliance against a different list of tick-boxes.

The Shifting Profile of Pre-Packs

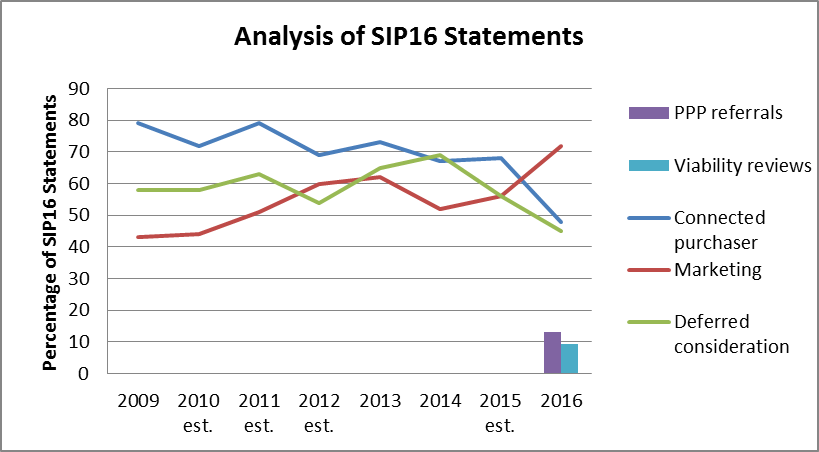

Probably the main difference between the old and the new SIP16 was the introduction of the “marketing essentials”, with the clear message that an absence of marketing should most definitely be the exception. Has the new SIP16 pushed up the frequency of marketing?

I certainly think that the SIP16 pressure has influenced attitudes towards marketing, as this graph indicates. Even in cases where the offer on the table looks too good to beat, I suspect that many view some marketing effort as essential to shield one from criticism. I doubt that safety-blanket marketing in these cases increases realisations and it will increase costs, but if it answers the sceptics’ questions about possible undervalue sales, then it seems to have everyone’s blessing.

Then again, perhaps I am being unfair: is it merely coincidental that the graph above shows that, as the frequency of marketing has increased, the prevalence of connected party purchasers has taken a dive? Could it be that increased marketing has widened the pool of potential purchasers, resulting in more occasions when connected interested parties lose out to the competition?

I am surprised that no one (as far as I have seen) has connected these two trends with this simple cause-and-effect explanation. Rather, perhaps I am not the only person who suspects that the fall in the number of connected purchasers is more a consequence of the new SIP16 pressures on connected party pre-packs, including the pressure to apply to the pre-pack pool. As revealed in its 2016 Review, the Pre Pack Pool is evidently of this view:

“It may be that the introduction of the Pool and the wider post-Graham reforms have deterred some connected party pre-packs from being proposed in the first place.”

But what has replaced these pre-packs? Are connected party sales avoiding the SIP16 obstacles altogether?

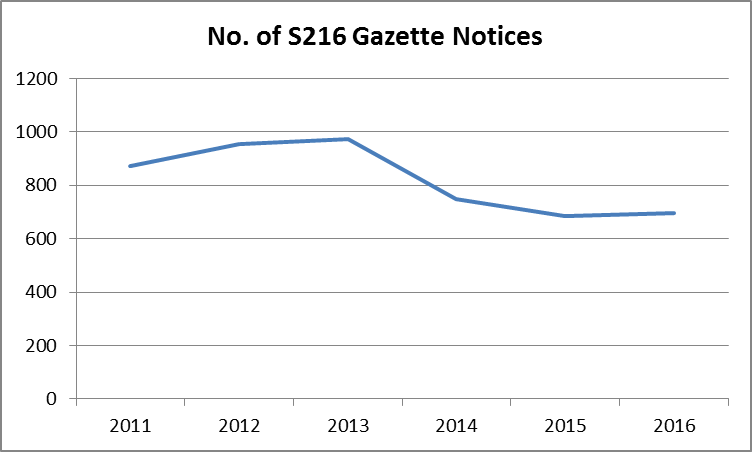

Perhaps hurdles are being overcome by having connected party sales accompany liquidations instead of Administrations. Well, I was surprised to discover that the numbers of Gazette notices for S216 re-use of a prohibited name do not follow a trend suggesting more sales in liquidation:

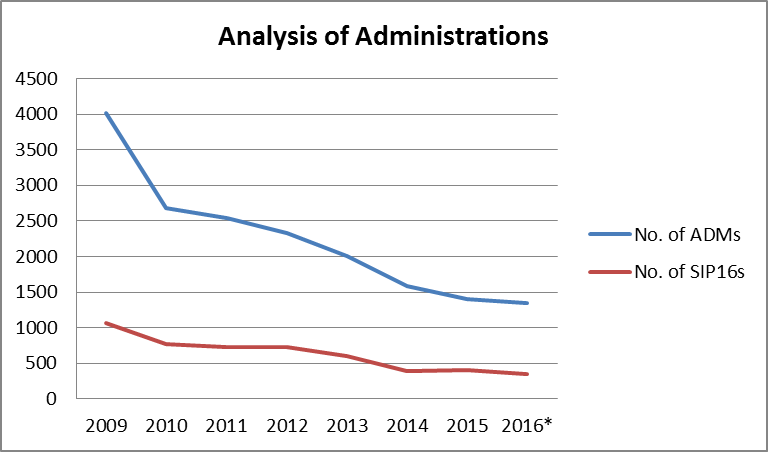

So could it be that Administration sales are being shifted out of the pre-pack definition either by being completed before Administration or perhaps negotiations are not starting until after appointment? This doesn’t ring true either: SIP16 statements as a percentage of the total number of Administrations has been fairly steady since the introduction of the Pool (2015: 29%; 2016: 24%):

* The SIP16 review actually covered 14 months, but for the purpose of this graph the number has been pro rated for 12 months.

Although the number of Administrations continues to fall, I find this picture encouraging: at least the SIP16 and Pool pressure does not seem to be persuading people to find ways around the measures. Pre-packs have a role and it seems that IPs are sticking with them.

Is the Pre Pack Pool making its mark?

In light of the second-hand warnings I’ve heard over the past years about how strongly the Insolvency Service feels about the need for IPs to embrace the Pool, I found the Service’s annual review surprisingly dead-pan. In contrast, the ICAEW’s release on the subject stated that the number of referrals to the pool was “disappointingly low”.

However, the ICAEW was relatively subtle about IPs’ role in the referral process: “the aim of the pool is to increase transparency and confidence around prepacks and low level use of the pool is unlikely to achieve that. We know you can’t compel a connected party to approach the pool but encouraging them to do so supports the overall aim of the pool”. I found the Pre Pack Pool less subtle: “the insolvency profession and creditors have important roles to play in ensuring connected party purchasers are informed of the option to use the Pool and putting pressure on them to do so”. How does the Pool expect IPs to “put pressure” on potential purchasers, I wonder.

The Pool also acknowledges that “creditor awareness of the Pool has been low and few have taken the time to read through administrators’ reports”. On the other hand, they report that “those connected party purchasers who have used the Pool have said it has been an important step in building credibility and trust in the ‘NewCo’ among creditors”. The Pool’s Review does not elaborate, but there are some interesting quotes in an article written by Stuart Hopewell, director of Pre Pack Pool Limited, and David Kerr, IPA’s Chief Executive, for Credit Magazine in November 2016 (www.insolvency-practitioners.org.uk/download/documents/1467).

As shown on one of the graphs above, 13% of all pre-packs were referred to the Pool. This represents 28% of all connected party pre-packs. Personally, I’m surprised it was that many! My personal view is that those who find this uptake disappointingly low had unrealistic expectations.

The Performance of the Pool

Given that referral to the Pool is voluntary, personally I wasn’t expecting any negative decisions to emerge. After all, if you didn’t have to sit an exam, you wouldn’t do so unless you were certain of passing it, would you? I was wrong…

The breakdown of the Pool’s opinions over the 14 months to the end of 2016 is as follows:

- 34 referrals: the case for the pre-pack is “not unreasonable”

- 13 referrals: the case is “not unreasonable but there are minor limitations in the evidence provided”

- 6 referrals (although 4 were a group of connected companies): the case for the pre-pack is “not made”

I appreciate that the Pool doesn’t want to give away its secrets, but unfortunately the Review gives nothing away about what factors tipped the balance or indeed how they measure a good pre-pack from the bad. The author ends the Review by stating that “hopefully referrals to the Pool will increase in 2017 as stakeholders become more familiar with the way it works and the reassurance it provides”, but without more feedback than simple statistics I cannot see this happening.

The Future of Pre-Packs

As we know, the Small Business Act included a reserve power to legislate the operation of pre-packs, with a sunset clause ending in May 2020. The Service’s Review continued its dead-pan mood, simply stating that they would carry out an evaluation “in due course”.

The Pool seemed barely more enthusiastic, simply stating in its Review that “it would be a shame to lose” pre-packs.

The Future of the Pool?

Back in May, the Times reported (https://goo.gl/QRcVZc) that Frank Field, Labour MP and Chair of the House of Commons’ Work & Pensions Select Committee, found the number of referrals to the Pool “deeply worrying” and he raised the prospect of the Committee scrutinising the Pool after the election. Sir Vince Cable also said that the number of referrals raised “worrying questions” and said that moves should be made towards making Pool referrals mandatory.

The Pre Pack Pool may be contemplating how to enlarge its role, but not necessarily with mandatory pre-pack referrals in mind. In the Credit Magazine article mentioned earlier (www.insolvency-practitioners.org.uk/download/documents/1467), Stuart Hopewell and David Kerr considered the extension of the Pool’s remit in the context of the revision of SIP13, suggesting “perhaps there is a role for the Pool to represent [creditors’] interests in all connected sale situations?” Although I continue to be concerned that much of the media outrage at connected party sales is levelled at the liquidation equivalents of pre-packs, surely the Pool must first provide convincing evidence that it is achieving the objective for which it was created before we seek to cast its net farther afield.

Are we to conclude that Hopewell/Kerr’s perception is that SIP13 sales to connected parties is an issue and having an independent review will regulate these sales? I am not aware of any research into whether Liquidation connected party sales need regulating, so it would seem again that the tide is pulling us to tackle perceptions. Considering that the regulatory objectives include “promoting that maximisation of the value of returns to creditors” and encouraging IPs to provide “high quality services at a cost to the recipient which is fair and reasonable”, I struggle to see how these objectives are met by contributing further to this expensive over-regulated PR exercise.