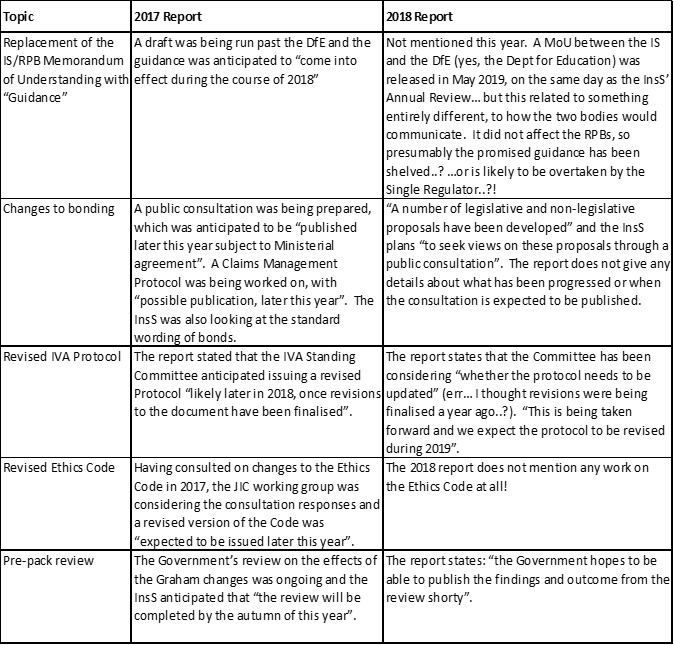

The new IVA Protocol is half a world away from its predecessor. In most respects, the changes are welcome. While Dear IP highlighted the main changes, many more adjustments are hidden away in the detail. The new template Annexes have also added lots more items worthy of a blog post.

In this post, I’ll explain the changes to the Proposals themselves and the Standard Terms and Conditions (“STC”). In the next blog, I’ll look at the other Protocol changes around dealing with debtors and introducers etc. and how to administer the IVA.

In this post, I look at:

- What changes from the April 2021 version were slipped in on 2 August 2021

- The ambiguities around the new home equity provisions

- Inconsistencies between the Proposal template annex and the Protocol/STC

- A host of small, but not inconsequential, changes in the STC

I am sorry for the length of this post! I didn’t want to miss anything out that could trip you up.

The new Protocol and associated docs are available from: https://www.gov.uk/government/publications/individual-voluntary-arrangement-iva-protocol

Where did the April-21 versions go?

The new Protocol and STC were originally released on the .gov.uk website on 29 April 2021. Dear IP 126 announced that the new Protocol etc. could be used immediately and that they would become mandatory for all new Protocol-compliant Proposals issued to creditors after 1 August 2021.

Then, on 2 August 2021, the April Protocol and STC were replaced on the .gov.uk website by amended versions.

In some respects, this was welcome – the InsS managed to fix some inconsistencies that I was trying to find the time to write to them about. However, what I cannot fathom is why they removed the April 21 STCs.

The many Covid-19 changes to existing IVAs announced by the IVA Standing Committee give me the impression that the Committee considers STCs to be moving feasts in any event, able to be changed unilaterally simply by saying it is so, much like a bank announces changes to the terms of its products. Guys, I don’t think that’s how it works. Surely an IVA must be administered according to the terms agreed by the debtor and the creditors; you cannot sneak in changes to the STCs without approval of the parties.

The new STCs are whizzy, containing hyperlinks that take you to other relevant clauses. Therefore, I wonder what firms did when they issued IVA Proposals in May, June and July. Did they reproduce the April 21 STCs on their own websites and/or circulate them to the debtors and creditors… or did they simply provide a link to the .gov.uk version? If they did the latter, then it will not be easy to track what STCs had been incorporated into which IVAs.

Given that it is evident the Insolvency Service has no qualms about slipping in changes to the STC published on https://www.gov.uk/government/publications/individual-voluntary-arrangement-iva-protocol/iva-protocol-2021-annex-1-standard-terms-and-conditions, it seems essential that IP firms reproduce the STC on their own website so that they – and the debtors and creditors – can have some certainty about which terms apply in each case.

Were the changes to the 2 August version material?

Well firstly, the Protocol itself doesn’t form a part of the IVA, so the changes there have no effect on IVAs proposed.

The STC changes were, as Dear IP 133 had announced:

- “Some minor amendments have been made to clarify the provisions on equity to reflect the position of the IVA standing committee”

The April-21 version stated that “if a re-mortgage can be obtained, the agreement will be automatically be (sic.) reduced to 60 months”. The Aug-21 version now reads: “if a re-mortgage cannot be obtained, the agreement will remain at 72 months. If equity is released the term will be reduced to 60 months”.

So yes, the Aug-21 version is certainly tighter – at least now the IVA duration won’t change just because a re-mortgage can be obtained – but I think it still leaves wriggle room as regards the amount of equity that must be released in order to cut 12 months off the IVA. Although the STC explain further what “equity to be released” means, I think a debtor could argue that they had met the terms simply by releasing some of the equity.

- “the redundancy clause in the protocol… has been updated to make it easier to interpret and understand”

Actually, this part of the Protocol has not changed, but the STC have. Now, the STC contain a detailed redundancy pay clause, which does not appear to change the debtor’s obligations from the April-21 version.

A change that is not listed in Dear IP 133 is the addition to the STC of:

- “You will be required to increase your monthly contribution by 50% of any increase in disposable income one month following such review”.

Unless this was included in the Proposal itself (and it is not included in the Protocol’s Annex 4, Proposal template), any PCIVAs issued with the April-21 STCs do not contain this requirement or anything like it. That could make for some interesting debates with debtors!

Material changes to home equity treatment

The changes between the 2016 and the Apr-21 STC are vast. The most material relate to the structure of IVAs where there is a property.

There are now three alternatives:

- Where the “available equity is below the de minimis amount”, the IVA will be drafted for a 60-month term and the equity effectively will be excluded from the IVA.

- Where the “available equity is above the de minimis amount but does not meet the current lending criteria for a potential re-mortgage as set out in annex 5 of this protocol”, the IVA will be drafted for a 72-month term and the equity effectively will be excluded from the IVA.

- Otherwise, the IVA will be drafted for a 72-month term; there will be a revaluation at month 54; and “if the second valuation confirms the equity position in the proposal” and if “equity is released”, then the term will reduce to 60 months.

The Protocol actually provides a fourth option:

- If option 3 is followed but equity release is not possible, then a third party may contribute a lump sum equivalent to 12 monthly payments and then the IVA can be concluded early. Unfortunately, however, this option is not covered in the STC, so unless IPs provide for this in the Proposal (and the Protocol’s Proposal template does not mention it), this approach will require a formal variation to be proposed to creditors.

What is the de minimis amount?

This isn’t defined in the STC. Personally, I think it should be: after all, what will happen if a future Protocol revision changes the amount?

The Protocol sets the de minimis at £5,000 (or £10,000 for a property jointly owned by two people proposing interlocking IVAs).

What is “available equity”?

Again, this is not defined in the STC. The Protocol states: “The value of the consumer’s equity will be considered de minimis if it is £5,000 or less when valued before the IVA proposal is put to creditors. The calculation should be based on 85% of the value of the property less any secured borrowings (e.g. mortgage). This means that the consumer will retain at least a 15% financial interest in the value of the property in all cases.”

Mmm… so “equity” doesn’t mean equity then. It means 85% of the equity.

Annex 5 of the Protocol also describes “anticipated equity”, which involves projecting both the property value (“using the simple interest formula at the date of the review”) and the mortgage position at month 54. It is not clear to me what should be done with this “anticipated equity” figure: I don’t think it is meant to determine whether the equity is above or below the de minimis, but is it intended to be the figure that the debtor must introduce to the IVA from month 54 if their IVA is to drop to 60 months’ long? Annex 7, the EOS template, doesn’t mention anything about projected equity values, so I really don’t know!

To be honest, although the STC include lots of statements about the upper limits of re-mortgage (e.g. a re-mortgage would bring the amount secured to no more than 85% of the total value of the property), I found it very difficult to identify what minimum payment would satisfy the “available equity” release condition.

What if the second valuation doesn’t “confirm the equity position”?

It isn’t clear what “confirm the equity position” means. How different from the equity position presented in the Proposal can it be before it is no longer “confirmed”? If it is way different, then can the IVA end at month 60 if nevertheless the available equity is released?

Presumably, this provision is meant to address situations where the equity turns out to be less than the de minimis at month 54. In this case, I would expect the IVA to drop to 60 months, but neither the STC nor the Protocol make this point.

At least the debtor should have a better idea of what is expected of them

The Protocol requires that “a copy of the calculations” – i.e. how the equity is proposed to be dealt with in the IVA – “should be provided to the consumer and also to all their creditors within the scope of the IVA proposal”.

Is the equity treatment clear in the Proposal template?

I have real problems with the Proposal template, which is provided as Annex 4 to the Protocol. As regards the equity treatment, the Proposal template gives me the following concerns:

- Para 6.2 states that the property will be valued in month 48, whereas the Protocol envisages month 54

- Para 6.3 states that the debtor “will make reasonable endeavours to introduce this sum into the arrangement” – it is by no means clear what “this sum” is

- Para 6.4 states: “Should I be unable to re-mortgage, I will continue to pay my IVA for the full 72 months, if I am successfully (sic.) and introduce equity my IVA will complete at month 60” – again, what amount of “equity” needs to be introduced (and of course the IVA won’t complete at month 60 unless the supervisor can wrap everything up immediately)?

Can the property be sold?

The Proposal template contains an interesting scenario. Para 6.5 states that, in the event that the debtor sells their home at any time in the IVA and pays in the sale proceeds less costs, “the additional remaining payments will no longer be payable into my IVA” even if the funds are insufficient to clear the debts and costs. So… a debtor with minimal equity sells their home early on in the IVA, pays in the small amount of sale proceeds… and then they are not required to pay in any more income-related contributions?!

I cannot see that this is an expectation of the Protocol. All it states is that, if a property is sold, then the proceeds of sale to the extent of settling the costs and debts in full – excluding statutory interest – shall be paid into the IVA.

Is statutory interest not payable for early completion?

Yep, that’s what the STC say. However, Para 5.1 of the Proposal template states: “The IVA will finish when the agreed level of payments have been made or I have paid creditors together with the costs of the IVA in full and with statutory interest”.

Are there other issues with the Proposal template?

Yep. I have lots of minor gripes (like reference to an irrelevant “3.1”), but some other material ones are:

- While it is reasonably complete as regards ticking off SIP3.1 and Rules’ matters, it does not flag up the SIP3.1 requirements to disclose the referrer, their relationship/connection to the debtor, or any payments to the referrer made or proposed, amounts and reasons.

- No monthly contribution amount is specified. It simply states (Para 5.1): “I will make monthly payments of my surplus income estimated at £X”. Odd!

- Para 7.3 strangely provides for a trust “in favour of the Supervisor” and states that the trust will end when the notice of termination is filed with the SoS. The STC state the trust will end earlier, i.e. when the certificate of termination is issued or, as regards assets not realised, when a bankruptcy order is granted.

- Para 7.11 states that late-proving creditors “will not be entitled to disturb dividends already paid but will be entitled to participate in future dividends”. The STC state that they will also be entitled to catch-up dividends.

Do these inconsistencies matter?

The STC state that, “in the event of any ambiguity or conflict between the terms and conditions and the proposal and any modifications to it, then the proposals (as modified) shall prevail”. So, yes, as always the Proposal takes precedence.

So, if the Proposal reverses or negates the apparent intended effect of the STC, can the Proposal be called Protocol-compliant? Surely not… except if the Proposal simply follows the Protocol’s Proposal template annex, then presumably it’s ok..?

Are IPs obliged to use the Proposal template?

It is not at all clear. The 2021 Protocol repeats the previous Protocol’s introduction that “Where a protocol IVA is proposed and agreed, insolvency practitioners and creditors agree to follow the processes and agreed documentation”. But, apart from the contents list, there is no specific mention in the Protocol to the Proposal template. Contrast this with specific reference to Annex 6, which gives examples of how an IP might comply with the Protocol’s new requirement to “set out details of how the funds received… will be allocated towards the costs of the IVA, together with a timetable and schedule of expected payments to creditors” (which interestingly is a document that is not mentioned in the Proposal template!).

So is the Proposal template intended to be just for guidance? Given its departures from the Protocol and STC, it cannot be intended to over-ride it all, can it?

What about the other templates?

The Proposal template states that attached is a “combined outcome and Statement of Affairs”. Annex 7 is clearly solely an estimated outcome statement, not a SoA.

Annex 3, which is an “example” letter to send to the debtor along with the draft Proposal, does not mention that a SoA (i.e. one that complies with the Act/Rules) is enclosed and there is no reference to a Statement of Truth, which the debtor is required to provide to the IP per R8.5(5). The letter also contains the old pre-29 June DRO thresholds.

Again, it is not clear whether IPs must use these templates. I also appreciate that it will be difficult to maintain templates to deal with changes in legislation or SIPs… but, hey, that’s what we all have to do, isn’t it?

Some things never change

One of the obvious changes needed to the STC was to bring it into line with the 2016 Rules as regards the various decision procedures. Way back in April 2017, Dear IP 76 had expressed the Insolvency Service’s expectation that supervisors “take advantage of the new and varied decision making procedures that are available under the Act as amended and the 2016 Rules”.

Did someone forget this expectation? The new STC still refer solely to “meetings of creditors” that may be called during the course of the IVA. As the STC state that they be called “in accordance with the Act and the Rules”, we are talking about only virtual meetings here. What is evident, however, is that it does not include electronic or correspondence votes.

Other STC changes

There are some relatively minor changes introduced by the new STC – I would love to give you paragraph references, but crazily the STC no longer have para numbers!

- Unsurprisingly, the old STC that supervisors can make a reasonable charge for variations has gone.

- The STC state that a completion certificate “will be issued within 28 days of all payments and obligations being satisfied”, although the Protocol states that the completion certificate should be issued within 3 months. Both the STC and Protocol provide a long-stop date of 6 months.

- The concept of a completion certificate where there has been substantial compliance has been ditched.

- The liabilities can now be up to 25% more than those estimated in the Proposal before it is considered a breach (the old STC provided for a 15% limit).

- A Notice of Breach will now always provide a timescale of one month to remedy and/or explain a breach (the old STC allowed the supervisor’s discretion to set a timescale of between one and three months). Now, a remedy can include proposing “a reasonable plan to remedy” the breach, which may be useful, although of course some proposals will still need to be varied formally.

- All trusts will end on issuing a certificate of termination or completion (the old STC were silent).

- A variation to reduce contributions can only be proposed in the first 2 years of the IVA “if evidence can be provided to creditors that the supervisor could not have reasonably foreseen such a change in circumstances at the start”.

- Interestingly, “if you cannot reach agreement with the supervisor in respect of your obligation to contribute additional income, then the supervisor has the discretion to issue a notice of breach”… or not.

- Oddly, the STC no longer describe any means for changing supervisors except by a block transfer order (or removal by a creditors’ decision). Presumably, though, a switch may still be proposed by variation. Para 2.8 of the Proposal template, however, does provide a simple: any “vacancy may be filled by an employee of the same firm who is qualified” as an IP, although I’m not sure if this over-rides the requirement for a court order or creditor decision appointing them.

- The requirement to register a restriction on a property has been removed from the STC. It is, however, still required under the Protocol, so you will need to make sure that it is included in your Proposal template (it is in the Annex 4 template).

- Creditors now only have 2 months to submit a claim, rather than the old 4 months.

- The supervisor now has discretion to admit claims of £2,000 (up from £1,000) without a PoD or claims that do not exceed 125% (up from 110%) of the amount listed in the Proposal without additional verification… with the new condition that this cannot “result in a substantial additional debt being admitted” – I’m not sure how this would be measured.

- Although both old and new STC state that all payments into the IVA “are intended to be used to pay dividends” and costs, now there is no limit on the surplus funds at the end of the IVA that will be returned to the debtor (it used to be £200 max.).

- I’m confused about the HMRC-specific requirements: they state that HMRC’s claim will include self-assessment tax arising in the tax year in which the IVA is approved (less payments on account), but then they state that the debtor “will be responsible for payment of self-assessment/NIC on any source of income that begins after the date of approval”, but then also that any “monthly charge for income tax/NIC as it appears in the income and expenditure statement” must be paid into the IVA for the rest of the tax year after approval of the IVA.

The consequences

All these intricate changes will complicate systems and procedures, as you will need to be alert to which terms apply to which IVAs you’re administering. As you can see, it would also be valuable to refresh your Proposal template to ensure that it corresponds with the new STC, plugs the gaps and eliminates ambiguities.

If you do choose to use the Protocol’s Proposal template, I recommend that you give it some tweaks to make sure it is SIP3.1-compliant (as well as tailored to your own practices, as some clauses are quite bespoke) and that it does not stray far from the new Protocol and STC.

More changes

These are only Protocol changes affecting the Proposal and STC. In the next blog, I’ll look at the other changes including new requirements as regards advising debtors and liaising with introducers.