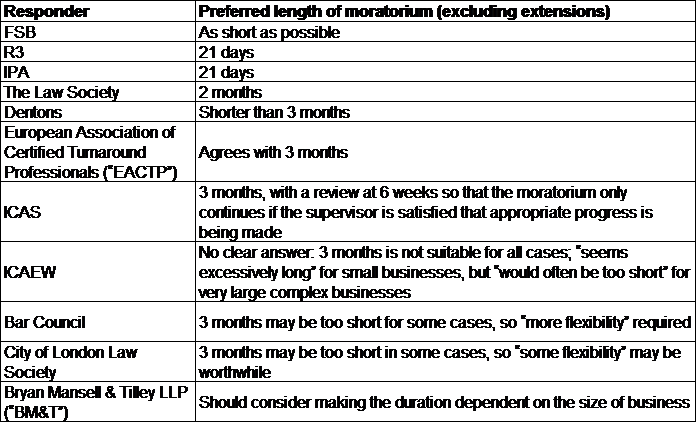

The Insolvency Service’s report on the 2016 Rules review contains some interesting gems. It’s a detailed report, which demonstrates they have scrutinised the consultation responses. The result is a list of proposed fixes to the Rules – most are welcomed, a few are alarming.

In this blog, I describe what I found was the most surprising and alarming statement in the report. It relates to the age-old question: is a paid creditor still a creditor? The report’s statement is surprising, as it is the polar opposite of a comment published by the Insolvency Service 5 years’ ago. And it is alarming because the report states merely that the Rules need to be made “clearer”, which suggests that we have all been misinterpreting the Rules over the past 5 years. But hey ho, we’re only talking about fee-approval and Admin extensions!

The Insolvency Service’s report is available at: https://www.gov.uk/government/publications/first-review-of-the-insolvency-england-and-wales-rules-2016/first-review-of-the-insolvency-england-and-wales-rules-2016

Is a paid creditor still a creditor?

If a creditor’s claim is discharged (and not subrogated to the payer) after the start of an insolvency proceeding, should that creditor still be treated as a creditor for decision procedures and report deliveries?

Before I left the IPA in 2012, the question began to be discussed at the JIC. It turned out to be a hotly debated topic and I never did learn the conclusion. I’d always hoped that there would be a Dear IP on the subject to settle the matter once and for all (subject to the court deciding otherwise, of course). It was such a live topic at that time that surely the 2016 Rules were drafted clearly, weren’t they?

The general principle?

I had heard a rumour long ago that the Insolvency Service’s view was once-a-creditor-always-a-creditor. I understood that the basis for this view was that creditors are generally defined as entities who have a claim as at the relevant date, so the fact that the creditor’s claim may have been discharged later does not change their status as a creditor.

Of course, this doesn’t work if, after the insolvency commences, the creditor sells their debt (or it is otherwise discharged by a third party): the purchaser/settlor tends to acquire the creditor’s rights, so the original creditor would no longer be entitled to a dividend or to engage in decision procedures – there are Rules and precedents to address these scenarios.

I can see where this view might come in handy, e.g. where an office holder had already paid creditors in full and only afterward realises that creditors have not yet approved their fees.

However, this view always seemed illogical to me: why should a paid creditor be entitled to decide matters that no longer affect them, e.g. the office holder’s fees or the extension of an Administration? Indeed, some paid lenders refuse to engage where their debt has already been discharged, even though an Administrator may need all secured creditors’ consents to move forward.

Setting aside this issue, it could be argued that in some respects the 2016 Rules support a once-a-creditor-always-a-creditor view. For example, R15.31(1)(c) states that in CVLs, WUCs and BKYs, a creditor’s vote is calculated on the basis of their claim “as set out in the creditor’s proof to the extent that it has been admitted”, which could indicate that post-commencement payments are ignored for voting purposes.

But then what about R14.4(1)(d), which states that a proof must:

“state the total amount of the creditor’s claim… as at the relevant date, less any payments made after that date in relation to the claim… and any adjustment by way of set-off in accordance with rules 14.24 and 14.25”?

Is the “claim” the original sum or the adjusted sum? If, for the purposes of identifying the “claim” for voting purposes, conveners are supposed to ignore post-commencement payments made, then doesn’t R14.4(1)(d) (and R15.31(1) – see below) mean that they should also ignore any set-off adjustment? That doesn’t make sense, does it?

Administrations are always “special”, aren’t they?!

R15.31(1)(a) provides that creditors’ claims for voting purposes are calculated differently for ADM decision procedures. It states that in ADMs creditors’ votes are calculated:

“as at the date on which the company entered administration, less (i) any payments that have been made to the creditor after that date in respect of the claim, and (ii) any adjustment by way of set-off…”.

This seems pretty unequivocal, doesn’t it? A paid creditor would have no voting power in an ADM decision procedure.

It is not surprising therefore that R15.11(1) provides that notices of ADM decision procedures must be delivered to:

“the creditors who had claims against the company at the date when the company entered administration (except for those who have subsequently been paid in full)”.

So the natural meaning of these Rules seems to be that paid creditors have no voting power and therefore do not need to be included in notices of decision procedures. This seems logical, doesn’t it?

What about prefs-only decision procedures?

These Rules led me to ask the Insolvency Service via their 2016 Rules blog: what is the position where an Administrator is seeking a decision only from the prefs, especially where those creditors also have non-pref unsecured claims? Do the Rules mean that, where a pref creditor’s claim has been paid in full, the pref creditor is ignored for the prefs-only decision procedure?

Or does the fact that the creditor hasn’t actually been “paid in full” because they have a non-pref element mean they should still be included in the prefs-only process? And does that mean that, per R15.31(1)(a), they would be able to vote in relation to their non-pref claim?

Yes, I know this would seem a perverse interpretation, but it seemed to me the natural meaning of rules that were not designed to apply to a prefs-only process.

The Insolvency Service’s view in 2017

The Insolvency Service’s response on 21 April 2017 (available at https://theinsolvencyrules2016.wordpress.com/2016/11/30/any-questions/comment-page-1/#comments – a forum on which the Service aimed to “provide clarity on the policy behind the rules”) was:

“Our interpretation is that 15.3(1)(a) (sic) would lead an administrator to consider the value of outstanding preferential claims at the date that the vote takes place. This would only include the preferential element of claims, and if these had been paid in full then the administrator would not be expected to seek a decision from those creditors.”

Now: the Government’s “long-standing view”

However, the Insolvency Service’s Rules Review report (5 April 2022) states:

“Several respondents asked for clarification on the position of secured and preferential creditors that had received payment in full. It has been the Government’s position for some time that the classification of a creditor is set at the point of entry to the procedure and that this remains, even if payment in full is subsequently made. We believe that to legislate away from this position could cause more problems than it would seek to solve. Accordingly, the Government has no plan to change its long-standing view on this matter. We will amend rule 15.11(1) to be clearer that where the Insolvency Act 1986 or the Rules require a decision from creditors who have been paid in full, notices of decision procedures must still be delivered to those creditors.”

Wow! If only the Insolvency Service had published the Government’s long-standing view 5 years’ ago, before all those fees had been considered approved by only unpaid prefs or secureds!

Is it only a R15.11(1) issue?

The Service’s report makes no mention of the voting rights of paid prefs. So does this mean that paid prefs should receive notice of decision procedures, but, in line with the Service’s statement in 2017, they have no voting rights? Or do they think that R15.31(1)(a) also needs to be changed?

And what about paid secured creditors? They’re not involved in decision procedures at all, so R15.11 is irrelevant where an Administrator is seeking a secured creditor’s approval or consent.

What is a “secured creditor”?

A secured creditor is defined in S248 of the Act as a creditor “who holds in respect of his debt a security over property of the company”. “Holds” = present tense. If a secured creditor no longer holds security over the company’s property at the time when an Administrator seeks approval/consent, are they in fact a secured creditor?

It seems to me that, if the Service wishes to amend the Rules to make them clearer as regards the Government’s position, they may need to look at amending the Act too.

The consequence of a clarification of the Rules

If the report had stated that the Service intended to change the Rules to give effect to the Government’s view, I would not have been so alarmed – that would be a problem for the future. But they have said that they want to make the Rules “clearer”. This suggests that they believe the existing Rules could be interpreted to give effect to the Government’s view. In that case, are we expected to apply the existing Rules in the way that this report describes?

And what about all the earlier cases in which paid secured or pref creditors’ approvals were not sought? What effect does this have on previously-deemed approved fees, extended Administrations and discharged Administrators?

And what does this approach achieve? Are IPs really expected to seek approvals/consents from paid creditors, most of whom have no theoretic, or even real, interest in the process? Why should paid prefs get to decide, even if they have non-pref unsecured claims, when no other unsecured creditors have this opportunity?

Are the ADM Para 52(1)(b) Rules fit for purpose?

I have often blogged that I think the Rules around the consequences for Para 52(1)(b) ADMs are confused and illogical. The Insolvency Service acknowledged some issues in the Rules Review report:

“Some respondents raised issues related to administration cases where statements had been made pursuant to paragraph 52(1)(b) of Schedule B1 to the Insolvency Act 1986, highlighting the difficulties that can sometimes occur when only secured and/or preferential creditors need to be consulted on certain matters under the Rules. It is clear that in some cases engagement with this smaller group of creditors can be difficult. However, we consider that the overall efficiencies provided for by the Insolvency Act and Rules across all such cases outweigh the difficulties that can occur in a minority of them.”

“The overall efficiencies”? Is the Insolvency Service saying that, because it is useful in many cases not to have to bother with non-pref unsecureds, this outweighs the issues arising in a minority of cases? If that’s true, then why not roll out this alleged more efficient process across all insolvency case types..?

The advantage of HMRC pref status?

Ok, a silent secured creditor can be a real headache and a silent paid secured creditor is going to be particularly reluctant to lift a finger. But now that HMRC is a secondary pref creditor in most cases, at least this eases the problem of getting a decision from the prefs, doesn’t it?

I understand that HMRC is still acting stony in the face of many decision procedures. Oh come on, guys! If you want IPs to waste estate funds applying to court, you’re going the right way about it.

Other issues with the Rules Review report

This is only one of a number of issues I have with statements in the report. In the next article, I will cover some others as well as highlight some items of good news for a change.

And apologies for my silence over the past months: an extremely busy working season and an unexpected health issue sapped me of my time and energy. Last August, I had planned on covering other effects of the IVA Protocol – this will emerge one day.