I believe we can be proud of R3 and the RPBs. Given only 6 weeks for the Government’s summer consultation, they generated robust and reasoned responses with plenty of variation to evidence that each had been created independently of the others.

Having read every published response I’ve been able to find, I am left with a reasonably strong sense of consensus on many of the big questions. However, I suspect that not all will be welcome news to the Government or the Insolvency Service, so the question is: will they listen?

The original consultation, A Review of the Corporate Insolvency Framework, can be found at: https://goo.gl/Cf0LWK.

In this post, I pick through the 14 responses that I discovered, including those from bodies such as R3, some of the RPBs and turnaround professionals. I don’t envy the Insolvency Service’s job of working through 70 submissions.

A New Moratorium: why?

Almost everyone saw some value in the principle (if not in the detail) of the Government’s proposals to introduce new moratorium provisions, although several questioned the Government’s apparent motives: from the consultation document, it does seem that a desire to get the UK up the ladder of the World Bank’s “Doing Business” rankings is the main driver, which does not seem a sensible policy-making foundation.

Dentons solicitors believe that “the UK has one of the most flexible insolvency regimes, unburdened by high costs and lengthy court procedures and, perhaps most importantly, one of the best recovery rates for creditors worldwide”, so it is difficult to see what advantages the proposed new process will bring. The City of London Law Society went further by not supporting the wider moratorium proposals, failing to see how a potentially costly process that may not adequately protect creditors’ interests would be useful.

The FSB expressed concern at the apparent move towards a US-style Chapter 11 system, feeling that this shift “could result in the UK regime’s strengths being watered down for little demonstrable gain elsewhere”. Several noted that the absence of a specialist insolvency court was a serious obstacle in any attempts to move towards a workable Chapter 11 style regime.

Most struggled to see how the moratorium could be used successfully by SMEs. Even the turnaround professionals were forced to admit that “there will always be some businesses that are too small to avail themselves of such help”.

A few responders felt that more effort should be made to encourage directors to seek help early and the turnaround professional felt that the moratorium would be a useful tool in this regard.

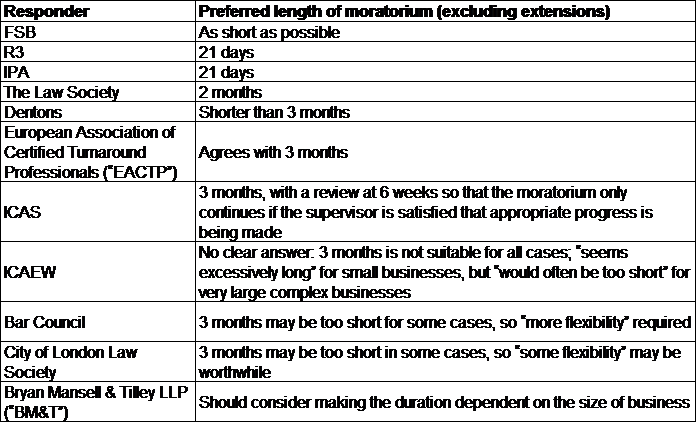

A New Moratorium: how long?

Here is a summary of the responses to the Government’s proposals for an initial 3-month moratorium:

It should be noted that many answers on this question were dependent upon other changes being made to the proposed moratorium set-up. For example, whilst the City of London Law Society felt that 3 months may prove to be too short for larger or more complex restructurings, it also recognised the risk that the extensive nature of the 3-month moratorium as proposed may “simply encourage directors to put off dealing with a company’s financial difficulties. This could, in turn, lead to creditor anger and frustration should the company’s financial position deteriorate during the moratorium period.”

A similar point was made by R3, which referred to the risk that “providing companies with an entire financial quarter free from creditor pressure could lead to ‘drift’ rather than action.” Instead, R3 stated, a shorter moratorium would make clear that it was the company’s ‘last chance’ to avoid insolvency, thus “requiring concentrated effort and a clear direction of travel”.

Will it simply be jobs for the boys?

The Government proposed that a new moratorium be introduced, which would be “supervised” by anyone with relevant expertise in restructuring who is also either an IP, solicitor or accountant.

However, in general the cry for supervisors to come only from the IP population was made loud and clear. You might think this was inevitable from the likes of R3 and the IPA, but even the accountancy and solicitor bodies were generally strong on this point.

- Not for solicitors?

The City of London Law Society pointed out that the SRA had only recently dropped regulating solicitors as IPs, so it would seem an odd development to have solicitors return to supervising something tantamount to an insolvency process.

- Not for accountants?

The ICAEW pointed to the facts that “accountant” covers a wide range of people and that there is already “a large pool of [insolvency] practitioners and a competitive market”, so it would seem an unnecessary risk to widen the pool to include others who are not subject to such heavy regulation as IPs. ICAS made a similar observation, noting its understanding that “at least one third of the [accountancy] sector in the UK has not undertaken any training or possess a formal qualification” and repeating its call on the Government to designate accountancy as a regulated profession.

- What about turnaround professionals?

Predictably, the EACTP and BM&T, turnaround consultancy, welcomed widening the role to more than just IPs, suggesting that the Certified Turnaround Professional qualification could qualify someone for the role.

Interestingly, these two responses were almost word-for-word the same in many respects, but they differed on one important point: BM&T believes that it is critically important for the supervisor to be clearly seen to be acting in the best interests of all stakeholders, whereas EACTP believes that the supervisor should act in the best interest of the company. I think this betrays one of the tensions in the proposals: is the moratorium intended for solvent companies that may be facing future insolvency or for insolvent ones? The City of London Law Society noted that the consultation document conflicts with the Impact Assessment on this fundamental point.

BM&T seemed alone in expressing the view that, in order to keep costs low, “supervisors should be subject to low levels of regulation”. I appreciate their point that the supervisor is not running the business, merely advising. However, given that a primary duty proposed for supervisors is ensuring that the moratorium – and not a formal insolvency process – remains appropriate, it does seem to me too high a risk activity to be largely unregulated. The ICAEW mentioned that, “if supervisors are not to be regulated persons, then greater court supervision may be required to minimise risks of abuse by directors and unfair prejudice of creditors”, which of course would increase costs and which in turn could have an altogether different impact on the World Bank rankings!

- The case for IPs

R3 believes that a clear commitment to protecting creditors’ interests is important. The Government’s proposals put creditors firmly in the back seat, offering them only the power to take court action to challenge the moratorium or their status as an essential supplier, a status assigned them by the moratorium company. If the company’s use of a moratorium to give it time to see a way out of its troubles is to earn the trust of creditors, the obvious choice is regulated IPs, and certainly not, as currently seems possible, the company’s in-house lawyer or accountant.

R3 reminded the Insolvency Service of the efforts the profession has made to tackle the problem of ambulance chasers and unregulated advisers. If not carefully structured and controlled, the moratorium could appear an attractive tool for abuse by some.

- A new professional?

Some responses highlighted the difficulty in ensuring that proposed supervisors meet the expertise criteria: the Government isn’t considering yet another different licence with potentially a whole new (and expensive) regulatory system, is it?

The IPA noted that the Government’s Impact Assessment made no mention of any costs of ensuring regulatory consistency in the event that the role is opened up to other professionals. It also reminded the Government of the new corporate-only insolvency licences, which would seem to lend themselves well to be used by non-IPs who want to develop in this area.

Consequences for Administrators

The Government’s proposals include two striking consequences for Administrations that are preceded by a moratorium:

- An IP who had acted as the company’s moratorium supervisor would be prevented from taking the appointment as Administrator (or indeed any other insolvency office holder); and

- The duration of the Administration would be 12 months minus the length of the moratorium.

Conflict of interest?

Few responded directly on this point. As you might expect, the ones that did respond fell into two distinct camps:

- There may be clear benefits in having the same person throughout, which would reduce costs, and the creditors should have a say in who they want as Administrator (ICAEW, ICAS, R3); and

- There would be a clear conflict of interest in having the IP supervisor also act as Administrator (EACTP, BM&T).

Personally, I cannot really see how the situation is different from a CVA Supervisor later being appointed as Administrator or Liquidator and I would expect the Insolvency Code of Ethics to be amended to treat the proposed subsequent appointment of a moratorium supervisor similarly.

Shorter Administrations?

Personally, I thought this second proposal was nonsense. Where is the logic behind giving Administrators less time to do their job simply because the company has had a moratorium? I appreciate that the perception may be that an Administration is all about exploring the company’s/business’ options, so if these are all but exhausted in the moratorium, then it should be time saved in the Administration. However, Administrators still need to get the job done and now must pay out any prescribed part dividend, which is by no means a 5-minute task. The ICAEW also made the point that at present the 12 months period “can be problematic, not least because of delays within HMRC and applying for extensions adds to work and cost”.

Although none of the consultation questions invited comments on this proposal, I was very pleased to see that several bodies managed to shoe-horn in their objections to shorter Administrations as a consequence of a moratorium. For heaven’s sake, Administrations are complex and costly enough as it is, please don’t make them any worse!

Having said that, the Law Society posed the sensible recommendation that the relevant date for excluding insolvency set-off and for voidable transaction claims should be measured from the start of the moratorium… although I would also suggest that, in that case, an insolvency office holder should be able to challenge certain dispositions occurring during a moratorium.

Directors’ liabilities

The consultation proposed that, provided the moratorium conditions continued to be met, directors would be protected from liability, e.g. in relation to wrongful trading, but that, should the conditions not be met and the moratorium fail, exposure for liability would resume.

This seemed a curious approach to me and the Law Society explained it well: “during a moratorium, directors will only be at risk once the company has reached the point at which they ‘knew or ought to have concluded that there was no reasonable prospect that the company would avoid going into insolvent liquidation’. Plainly, directors should also terminate a moratorium at, or before, that point, so that it is unnecessary to relieve the directors of liability whilst the conditions for a moratorium are maintained. Indeed, to do so would simply introduce unnecessary complexity into the law”.

The City of London Law Society also observed that suggesting that directors may avoid personal liability “could lead to inappropriate risk taking, particularly if directors believed that they could entirely rely on the views of the supervisor, rather than making their own assessment of the company’s prospects”.

Ranking of costs and expenses in the moratorium

Although a company would be required to have enough capital to discharge all debts incurred during the moratorium, what if the worst should happen?

Several responders agreed with the Government’s proposal that any unpaid debts incurred in a failed moratorium and the supervisor’s costs should enjoy a first charge in any subsequent insolvency (although there was no comment on the priorities between these categories).

However, R3 disagreed, noting that a company could stack up debts to connected parties during the moratorium, which would end up having priority, and so R3 believed that unpaid debts should rank alongside other claims in the subsequent insolvency. Personally, I don’t see that this potential abuse is sufficient reason to push moratorium creditors down the queue, especially in view of the other proposals regarding pressing “essential suppliers” into service during a moratorium.

The City of London Law Society also queried how it is proposed such costs and expenses would be approved for payment from a subsequent insolvency. Perhaps it would be something akin to the current pre-administration costs regime?

Several responders objected to the Government’s proposal that supplies during the moratorium should be paid for under the supplier’s usual terms of credit. BM&T made the connection that, if instead moratorium supplies are paid on a cash up-front basis, there should be no risk that debts would spill over into any subsequent insolvency.

Creditors held to ransom?

The “essential suppliers” proposals generated whole new lines of debate, such as the possible effects on the supplier’s trade credit insurance or debt factoring, which is material for another blog post.

Suffice to say, as worded in the consultation it seems that any supplier (…or only those with a contract? One example in the consultation is of a paper supplier) could be designated by the company as essential (by means of a court filing) with the result that the supplier would be required by statute to continue to supply on the existing terms, whilst its pre-moratorium arrears would be frozen, irrespective of the impact this might have on the supplier’s own solvency.

What’s wrong with the CVA moratorium?

The consultation claimed that the CVA moratorium is rarely used because it is limited to small companies. However, instead of proposing simply to widen the scope of the CVA moratorium (as ICAS has suggested), a new kind of moratorium is the proposal. This would be fine if the plan was simply to adapt the CVA moratorium to allow other restructuring solutions to flow from it, but the proposed new moratorium is different in many unconnected respects.

It is true that there are few CVA moratoria. Both the ICAEW and R3 suggested that the onerous responsibilities (and associated liabilities) of the CVA moratorium nominee deter use of the existing regime. Although we only have a skeleton proposal to judge at the moment, personally I don’t see that the new moratorium would deal with this obstacle any more successfully.

The ICAEW recommended that, to avoid any new moratorium suffering the same fate as the CVA moratorium, the reasons for its apparent lack of use should be analysed.

What’s wrong with CVAs?

As the only debtor in possession formal insolvency tool, you’d think that the Government might be interested in encouraging greater use of CVAs, but it seems to be missing the point.

The consultation stated that “the Government believes that the under utilisation of CVAs is largely caused by the inability to bind secured creditors”, however neither it nor its accompanying Impact Assessment provided any evidence to support this. The Impact Assessment stated that “the consultation will seek to understand fully the reasons behind” the under-utilisation of CVAs and the apparent fact that many fail (2014: 60%), but the consultation didn’t really address this at all. It simply stated that “many CVAs fail because of a failure to maintain agreed payment” – you don’t say!

R3 believes that “the most common reasons why CVAs fail is not because there is a problem with secured creditors but because the management is overly-optimistic in its financial assessment of the company, or the environment in which the company operates changes during the CVA.” The IPA makes a similar observation, suggesting that the CVA process is not at fault, but often the issue is with the underlying viability of the business. ICAS also reported that “anecdotally it is suggested that a significant proportion of CVA proposals will focus on financial/debt restructuring without addressing more fundamental and underlying operational restructuring or management change”.

In its response, R3 asked the Government to work with the profession and the creditor community to “to find ways to improve CVAs so that they can become a much more effective business rescue tool”, especially for SMEs, a request that also seems to have the support of the ICAEW and IPA.

And there’s much more

Some other meaty questions considered by the responders included:

- Do the Government’s proposals achieve the right balance of debtor-in-possession and creditor protection?

- If the balance swings too far away from creditors, as many responders fear, what will be the effects on lending?

- What exactly are the supervisor’s role and duties?

- How exactly should the moratorium entry criteria be defined and measured?

- How will notice of the moratorium be publicised or even should it be publicised?

- How would an extension to the moratorium be achieved and for how long should an extension be?

- Who would be required to provide information to creditors during the moratorium and what kind of information should be provided?

- Is there really a need to incentivise rescue funding, particularly by introducing contentious statutory provisions affecting existing secured creditors’ rights?

The consultation responses evidence that, within only a few summer weeks, a great deal of effort has been spent deliberating over the proposals, but the fun has only just begun.